Mastercard recently launched Agent Pay for Machines (AP4M), a payment system built for AI agents to transact on their own. The pitch is simple. Agents will not just recommend and book things for people. They will hand money to other agents and services, continuously, at a speed and volume no human checkout flow was ever designed for.

This is the part most founders are sleeping on.

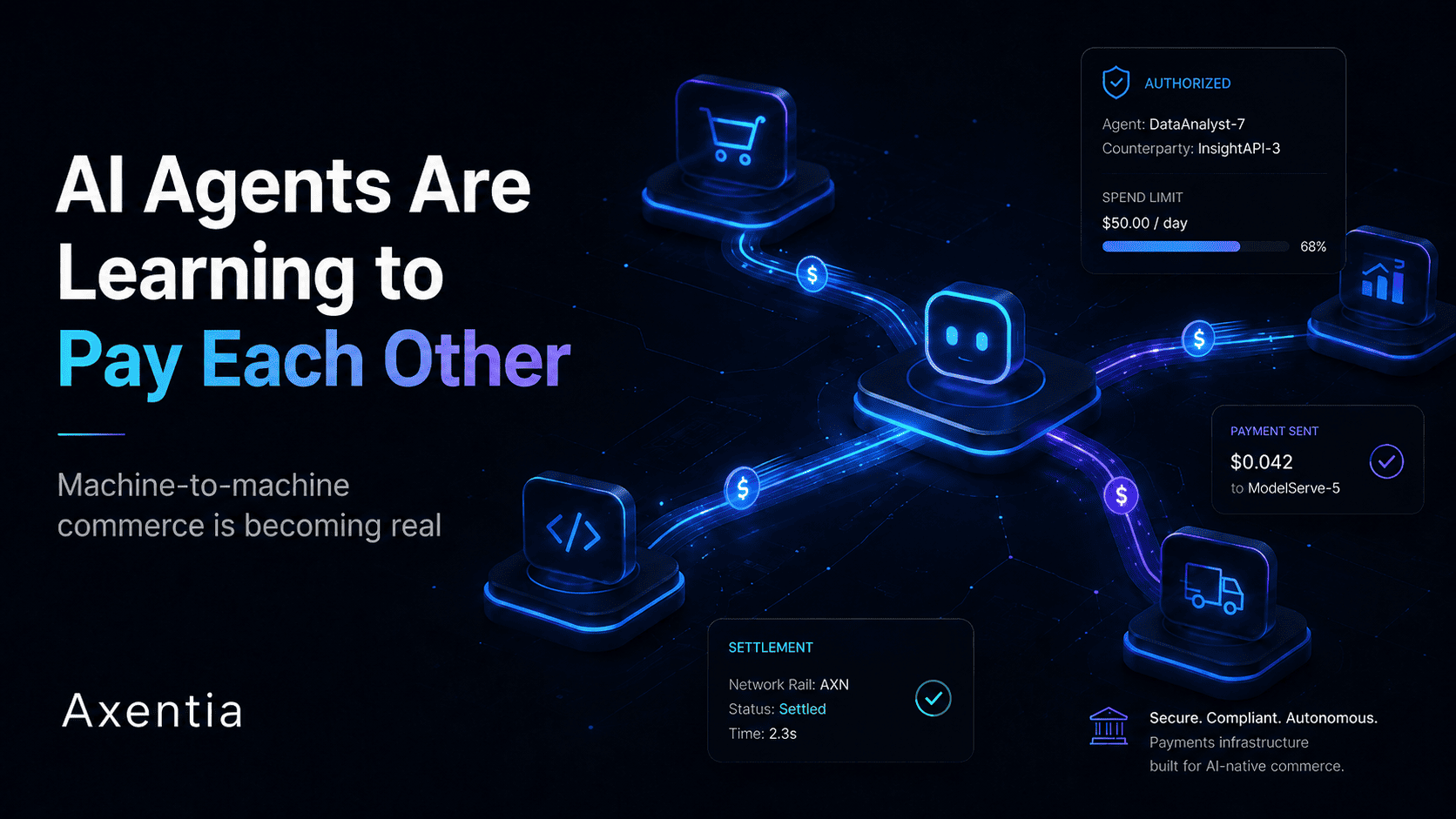

What Mastercard actually shipped

AP4M extends Mastercard's earlier Agent Pay program, which launched in 2025 to let verified agents pay on a consumer's behalf. The new version goes further. It targets machine-to-machine commerce: high-frequency, low-cost transactions, some worth fractions of a cent, running in the background between software systems.

It launched with more than 30 partners. The list mixes traditional processors like Stripe and Adyen with crypto-native firms like Ripple, OKX, Coinbase, and Tempo. That blend is the signal. Mastercard is hedging across card rails and blockchain rails because nobody knows yet which one wins for tiny, constant payments.

The whole thing rests on three pillars: proving an agent is authorized to spend, setting hard limits on what it can buy, and guaranteeing the money actually settles.

Why this matters if you are building a product

Mastercard's own example is worth sitting with. A founder opening a flower shop tells an agent to build the store's web presence. The agent buys a domain, picks a hosting plan, sources images, and wires up checkout, all inside a budget. One instruction becomes a chain of purchases executed across providers without anyone touching a card form.

Now flip it. If agents are buying, someone has to be selling to them. That someone could be you.

A product priced and packaged for an agent to discover, evaluate, and purchase on its own is a very different product than one built for a human clicking through a pricing page. Metered access to your data. Pay-per-call tooling. Services that quote a price and settle in milliseconds. These become viable business models the moment agents can pay reliably.

Payments are quietly becoming infrastructure

There is a reason a payments giant wants to disappear into the background. The companies that own the trust layer, the part that decides which agent is allowed to spend and how much, capture the value of every transaction that flows through it.

Mastercard is not alone here. Visa has its own agent protocol, Google and Shopify pushed a commerce standard, and Coinbase built one too. The standards war is on, and it will shape how money moves between machines for the next decade.

What to do about it

You do not need to integrate any of this tomorrow. You do need to ask one question. If a customer's agent, rather than the customer, showed up to buy what you sell, could it? For most products right now the answer is no. Closing that gap early is a real edge.

Agentic commerce is moving from slideware to live rails. The founders who design for it now will be the ones agents can actually pay later.

At Axentia we help founders figure out where AI agents fit into their product and build the integrations that make them real. If machine-to-machine commerce is anywhere near your roadmap, that is a conversation worth having.